Fintech CRO: Conversion Optimization for Financial Services Apps

Fintech apps convert by building trust, removing friction, and personalizing onboarding, KYC, and retention using data-driven UX and A/B testing.

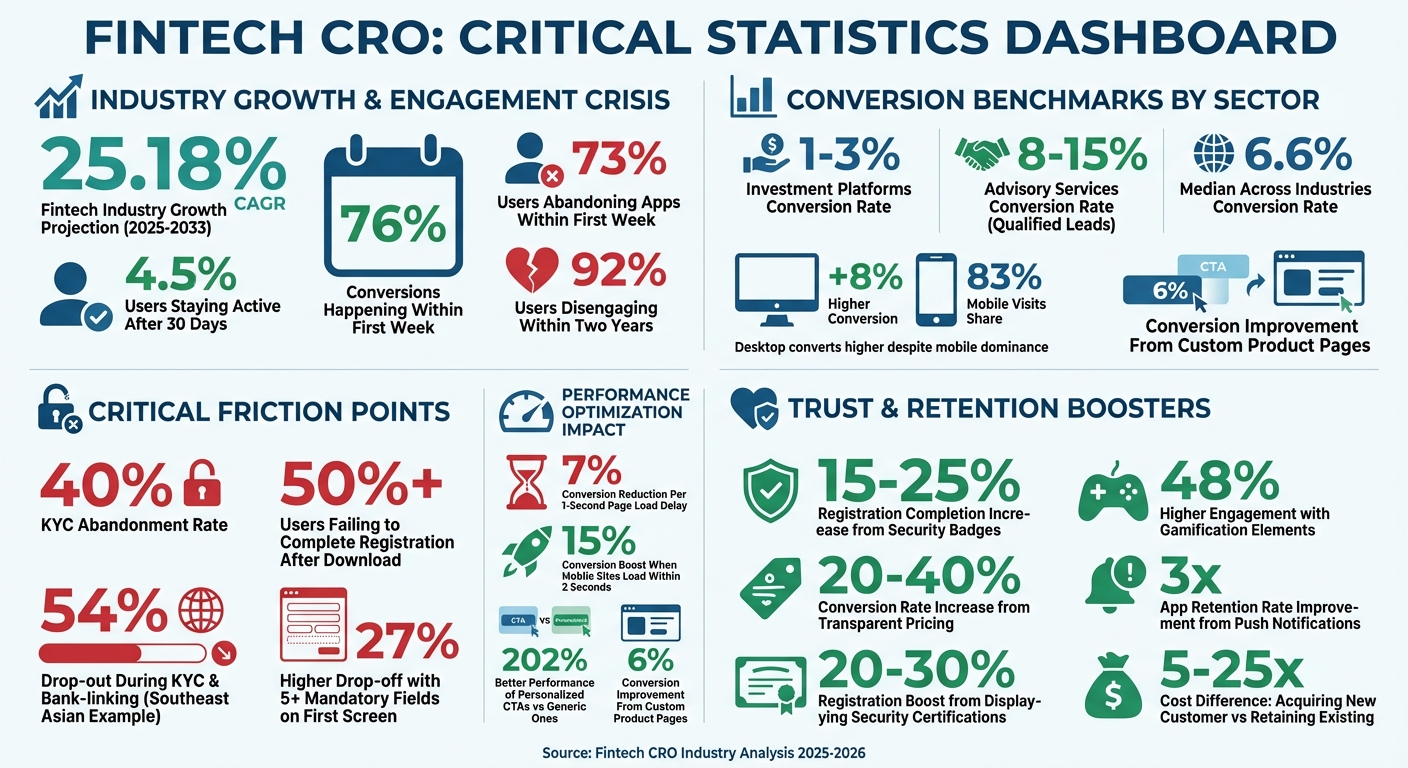

Fintech apps face unique challenges in improving conversion rates. Unlike e-commerce, fintech conversions involve sensitive, trust-based actions like account openings or loan applications. With only 4.5% of users staying active after 30 days and 76% of conversions happening within the first week, optimizing acquisition, onboarding, and retention is critical. Here's what you need to know:

- Key Stats: The fintech industry is growing at a projected 25.18% CAGR (2025–2033), but user engagement remains low. KYC abandonment rates can reach 40%, and a 1-second page load delay can reduce conversions by 7%.

- Metrics to Track: Focus on macro-conversions (e.g., account openings) and micro-conversions (e.g., starting a KYC form). Mobile sites that load within 2 seconds see a 15% conversion boost.

- Tools: Use analytics platforms like Mixpanel, Amplitude, and Heap to identify friction points. Complement with tools like Hotjar for heatmaps and Optimizely for A/B testing.

- Onboarding Tips: Simplify steps, use clear messaging, and offer "Save and Continue Later" options. Apps with fewer than five mandatory fields on the first screen reduce drop-offs by 27%.

- Retention Strategies: Behavioral triggers, push notifications (2–3 per week), and gamification can improve engagement. Personalized automation helped Niyo boost conversions by 40%.

- Building Trust: Display security badges, use biometric logins, and provide transparent pricing. Apps with upfront costs see conversion rates increase by 20%–40%.

- UX/UI Best Practices: Prioritize core actions, ensure thumb-friendly navigation, and use clear visual hierarchy. For instance, simplifying onboarding steps reduced drop-offs for PayUp.

Bottom Line: Success in fintech CRO relies on building trust, reducing friction, and personalizing user experiences. With the right metrics, tools, and strategies, you can drive meaningful growth in this competitive space.

::: @figure  :::

:::

Metrics and Tools for Measuring Conversion Rates

Core Metrics to Track

Understanding how to calculate your conversion rate is simple: divide the number of completed actions by the total number of users, then multiply by 100 [7][12]. But the real challenge lies in identifying the right actions to monitor for meaningful fintech CRO.

You’ll need to focus on two types of conversions: macro-conversions and micro-conversions. Macro-conversions are tied to revenue-driving actions, like opening an account or submitting a loan application. Micro-conversions, on the other hand, capture smaller engagement signals, such as using a mortgage calculator or starting a KYC form [7][1]. These micro-conversions are particularly useful for spotting where users show intent but encounter friction before reaching the main goal. For instance, if 1,000 users land on your pricing page but only 50 proceed to start registration, that 5% conversion rate could point to issues with messaging or trust.

Industry benchmarks help you measure your performance against others. Investment platforms typically see conversion rates between 1% and 3% [6], while advisory services can hit 8% to 15% for qualified leads [1]. Across industries, the median conversion rate stands at 6.6% [9]. Interestingly, while 83% of landing page visits occur on mobile, desktop users convert at rates that are, on average, 8% higher [9]. This highlights the need to optimize for both platforms rather than assuming success on one will translate to the other.

Breaking your user journey into stages can reveal exactly where drop-offs occur. Key metrics to track include app acquisition rates, registration completion times, KYC document rejection rates, and time-to-first-transaction for activation [6]. As Joe Pfeiffer, VP of Product at Northwestern Mutual, puts it:

"We almost take it for granted now that every new feature that goes out has analytics on it so we can quickly see if people use it or not" [3].

Other factors, like page load speed, also play a major role. Mobile sites that load within two seconds see conversion rates improve by 15% [6]. Additionally, personalized CTAs outperform generic ones by 202%, making segmentation and targeted messaging critical [6].

These metrics lay the groundwork for using advanced tools to turn data into actionable insights.

Tools for Tracking and Analysis

Once you’ve identified the key metrics, the right tools can help you analyze and act on them effectively.

Product analytics platforms are invaluable for fintech apps. Mixpanel, for example, focuses on event-based tracking, offering tools like "Flows" to visualize how users move through your app. It’s particularly useful for optimizing KYC funnels and cohort analysis [10]. Lemonade leveraged Mixpanel to grow its policyholders by 500% [10]. Vince Maniago, VP of Product Management at Empower, highlights its value:

"With Mixpanel, our decisions are backed by data instead of conjecture, meaning we can move forward with real product management work" [10].

Amplitude is another strong option, offering behavioral analytics and industry-specific benchmarks for acquisition, activation, and retention [11]. Its "Behavioral Graph" analyzes billions of user actions to identify what drives long-term engagement [11]. Meanwhile, Heap (now part of Contentsquare) automatically tracks every user interaction, making it easier to pinpoint friction points in complex funnels. Tyler Lane, Product Manager at OppFi, shares:

"Heap took it to a whole new level by showing us the specific points where our applicants experienced the most friction and required the most effort" [4].

Google Analytics 4 is essential for tracking traffic and source attribution, but it requires careful segmentation by device and user type to get meaningful insights [6][8][9]. For a deeper understanding of user behavior, qualitative tools like Hotjar provide heatmaps and session recordings. These tools can highlight areas of frustration, such as "rage clicks", where users repeatedly click on unresponsive elements [9].

Testing platforms like Optimizely and VWO allow you to run A/B tests on specific features. However, it’s crucial to use a test duration calculator to ensure your results are statistically significant (at least 95% confidence) before rolling out changes [9]. Combining quantitative data from analytics tools with qualitative insights from session recordings helps you understand both what users are doing and why they’re doing it.

sbb-itb-0499eb9

User Acquisition and Onboarding Optimization

Acquisition Strategies for Fintech Apps

Bringing in users for fintech apps is no small feat - it can cost 3 to 5 times more than in other industries. Acquisition costs often range between $200 and $2,000 per user, largely due to extended decision cycles (typically 3–6 months) and strict regulatory requirements that limit marketing options [13].

The best strategy? A mix of channels. Content marketing and SEO stand out for attracting high-quality users and delivering strong long-term returns. Meanwhile, paid search campaigns generate volume with moderate-to-high user quality [13]. Financial influencer campaigns are also worth noting, achieving 3–8% engagement rates, far surpassing the 0.5–2% seen in traditional financial ads [13]. As Charles Menke, COO at Wolf Financial, puts it:

"Fintech user acquisition requires balancing growth metrics with FINRA, SEC, and state regulatory compliance" [13].

Another effective tactic is using Custom Product Pages (CPPs) in the App Store. These allow you to tailor app messaging based on user intent. For instance, you can create one page focusing on "budgeting tools" and another on "investment options." This approach can improve conversion rates by nearly 6% [5]. Revolut took it a step further by localizing their App Store visuals. In Germany, they emphasized professional design, while in India, they highlighted security and savings to better align with local priorities [5].

Before asking users to sign up, show them the value your app offers. Features like interactive product tours, sample dashboards, or calculators can give users a hands-on preview, building trust before they commit to steps like KYC (Know Your Customer) or linking their bank accounts [14]. Once you've captured their interest with tailored messaging and fast load times, a smooth onboarding process becomes key to keeping them engaged.

Onboarding Best Practices

Getting users to install your app is only half the battle. The real challenge lies in turning that initial interest into active engagement. The numbers speak for themselves: over 50% of fintech app users fail to complete registration after downloading the app. Poor onboarding experiences can slash retention and transactions by as much as 50% [15][14]. For example, a Southeast Asian personal finance app found that 54% of users dropped out during the KYC and bank-linking steps [[17]](https://www.turingcorp.net/case-studies/strategies/6. [Summary] Stop KYC drop offs design an aha onboarding.html).

One major cause of drop-offs? Asking for too much information upfront. Apps that require more than five mandatory fields on the first screen see a 27% higher drop-off rate [15]. Breaking identity verification into smaller, manageable steps with clear progress indicators can help. Offering a "Save and Continue Later" option for document-heavy tasks is another way to keep users from abandoning the process [15][6]. For example, POSist increased demo requests by 52% by continuously A/B testing its digital interfaces [8].

Language also matters. Use clear, benefit-driven messaging instead of formal jargon. For instance, instead of saying "Submit KYC", try something like "We verify your ID to keep your account safe and comply with regulations" [14][15]. Displaying security certifications during onboarding can further reassure users, boosting registration completion rates by 20% to 30% [15]. Simplify the process even more by enabling one-click registration options using Google, Apple ID, or Facebook [15].

Behavioral analytics can also pinpoint where users get stuck. In June 2025, Indian mobile-first bank Niyo used this approach to deploy contextual nudges during the KYC stage, leading to a 23% increase in Day 7 retention [14]. BharatPe took a different route by integrating educational content about digital payments into their onboarding flow, which resulted in a 22% rise in weekly user registrations [19].

Timing is everything when asking for permissions. Don’t request access to features like the camera or location right after launch. Instead, wait until users naturally trigger a feature that requires it, such as scanning a check for camera access [16]. Offering pre-populated budget categories, interactive demo modes with sample data, or other value-first features can also create an immediate "aha" moment. This approach helps reduce churn, which affects 76% of mobile users within the first week of installing a fintech app [[17]](https://www.turingcorp.net/case-studies/strategies/6. [Summary] Stop KYC drop offs design an aha onboarding.html)[16].

Building Trust and Improving UX/UI

Trust Signals for Financial Apps

In the fintech world, trust is non-negotiable. With the average cost of a data breach hitting $5.72 million[20], showing users that their data is secure isn’t just a nice-to-have - it’s essential for your business.

The best trust signals are visible and interactive. For example, adding security badges during sign-up can increase registration completion rates by 15%-25%[20]. Biometric login options, like Face ID or fingerprint authentication, not only speed up access but also reassure users that security is a priority[21]. Alex O'Byrne, Co-founder of We Make Websites, puts it simply:

"Trust is the first principle of conversion"[20].

Fee transparency is another critical factor. Apps that clearly display costs upfront see conversion rates improve by 20%-40%[20]. Hidden fees are a major turn-off - users want clarity about what they’re paying before committing. Similarly, when requesting sensitive information like Social Security numbers or bank details, a brief explanation such as, "We need this information to comply with KYC regulations and secure your account," can help alleviate privacy concerns and reduce drop-offs[21].

Real-time transaction updates also play a big role in building trust. Providing clear status messages - such as "pending", "processing", "posted", or "failed" - helps users stay informed and avoid confusion about their account activity[18][22].

Social proof is another powerful tool. With 91% of consumers trusting online reviews as much as personal recommendations[20], showcasing authentic customer testimonials or ratings can significantly enhance credibility.

By incorporating these trust signals, fintech apps lay the groundwork for a user-friendly interface that drives conversions.

UX/UI Best Practices for Conversion

Once trust is established, a well-designed user experience (UX) and user interface (UI) can further strengthen user confidence. In fact, 89% of users say they would switch banks for a better user experience[21].

Start by simplifying the login process. Biometric authentication should be the default - it’s faster, more secure, and aligns with user expectations[23]. After logging in, displaying account balances and recent transactions immediately addresses users’ primary needs when opening a banking app[23].

Here’s an example: In 2025, Bitcoin of America worked with UX 4Sight to enhance their app’s design, focusing on navigation clarity and visual hierarchy. The results? A 67% boost in online account conversions and a 12% drop in bounce rates[25]. Abdul Suleiman, CEO of UX 4Sight, noted:

"Fintech design is unique because it blends intuitive user experiences with the highest standards of security and compliance."[25]

Keep in mind the Pareto principle: 80% of users interact with only 20% of features[23]. Instead of overwhelming users with options, prioritize core actions like checking balances, transferring money, and reviewing transaction history. For instance, PayUp, a financial startup, collaborated with Eleken in 2026 to simplify their onboarding process by breaking it into smaller, well-explained steps with helpful tooltips. This approach improved user understanding and reduced drop-offs during sensitive data collection[21].

For mobile apps - which more than 50% of banking customers rely on - thumb-friendly navigation is a must[25]. Placing key actions at the bottom of the screen ensures ease of use[24]. Additionally, offering a brief "undo" option after high-stakes actions, like transferring large sums, gives users a chance to fix errors without stress[21].

As Sophia Andrus from Eleken puts it:

"Clarity is not decoration. It's a form of respect for users' attention and emotional state"[21].

When users feel at ease navigating your app, they’re more likely to complete actions, stay engaged, and trust your platform over the long haul.

Retention and Lifecycle Monetization

User Retention Techniques

Getting users to download your fintech app is just the first step; keeping them engaged is where the real challenge begins. The numbers paint a stark picture: around 73% of users abandon fintech apps within the first week, and over 92% disengage within two years[26]. Considering that acquiring a new customer can cost 5 to 25 times more than retaining an existing one[26], focusing on retention isn’t just smart - it’s essential.

One of the most effective ways to combat churn is through behavioral triggers. These aren’t your generic reminders. Instead, they rely on real-time data to send timely and relevant nudges, like a notification about a paycheck deposit or a low balance alert[26][5]. For example, Niyo, a fintech startup, used personalized automation to address user pain points like high forex fees. The result? A 40% boost in conversion rates and a 12% re-engagement of dormant users[2].

Push notifications are another powerful tool - they can triple app retention rates[26]. But there’s a fine line: 78% of users say irrelevant or excessive notifications are a dealbreaker that leads to uninstalling apps[26]. The sweet spot? Limit notifications to 2–3 per week, unless users specifically opt for more. As Olabinjo Adeniran, a Senior Lifecycle Marketer, wisely notes:

"Testing is the bedrock of a solid lifecycle marketing professional. I always assume that I don't know - even when I think I know"[28].

Gamification can also work wonders. Apps that incorporate gamified elements, like savings streaks, achievement badges, or leaderboards, see 48% higher engagement rates[26]. For instance, Paysend, an international money transfer service, introduced personalized campaigns tailored to user segments in June 2025. This approach led to a 23% increase in repeat transactions and a 22% growth in weekly new-user registrations[2].

AI-driven personalization takes retention a step further. With machine learning, fintech apps can predict churn risks and respond with tailored content, such as customized investment tips or savings goals based on individual spending habits[26][8]. McKinsey highlights this growing expectation:

"71% of consumers expect personalized content from companies, and 67% feel frustrated when their interactions aren't tailored to their needs"[26].

Ultimately, strong retention strategies not only keep users engaged but also lay the groundwork for more effective pricing and monetization approaches.

Pricing and Monetization Strategies

Retention isn’t just about keeping users around - it’s also the foundation for driving revenue. Metrics like Average Revenue Per User (ARPU) and Customer Lifetime Value (LTV) link user engagement directly to financial performance, helping to justify acquisition costs.

Experimenting with pricing models can unlock long-term value. A/B testing freemium and free trial options, for example, can help determine which approach yields higher LTV[26]. Some fintech apps, like Robinhood Gold, have found success with tiered membership models that offer advanced features or better rates for a subscription fee[26].

Clear and upfront pricing is another critical factor. Apps that are transparent about costs can see conversion rates improve by 20%–40%. This transparency shouldn’t stop at the sign-up stage - users need to understand exactly what they’re paying for throughout their journey.

To make the most of retention efforts, fintech companies can use lifecycle scoring to identify and re-engage users before they lose interest[27]. Metrics like the DAU/MAU ratio (daily active users divided by monthly active users) can reveal early signs of disengagement, enabling targeted offers or re-engagement campaigns. In 2025, Anthem, an educational neobank, used behavior-triggered messaging and personalized offers to increase overall user transactions by 17%[2].

The shift from traditional Customer Relationship Management (CRM) to Client Lifecycle Management (CLM) is reshaping how fintech companies approach monetization[27]. Instead of treating acquisition, onboarding, and growth as separate steps, CLM integrates them into a seamless, ongoing process. This ensures every interaction supports higher conversion rates and maximizes revenue opportunities.

How Moniepoint tripled conversion rates with Mixpanel insights

::: @iframe https://www.youtube.com/embed/QbGlwun30zo :::

Key Takeaways

Boosting conversion rates in fintech isn't just about numbers - it's about earning trust, removing obstacles, and creating a personalized experience for every user. Unlike typical SaaS, fintech asks users to entrust you with their money, making trust-building absolutely critical.

Trust signals matter. Displaying security badges like SOC 2, PCI DSS, and FDIC, along with being upfront about fees, can significantly increase conversions. Speed also plays a big role - mobile pages need to load in under two seconds to keep visitors engaged and reduce bounce rates[6][1]. These steps lay the groundwork for a smoother user journey.

Onboarding can make or break retention. KYC verification stages often see abandonment rates as high as 40%[6]. However, using OCR technology for document uploads and letting users save their progress can win back up to 52% of those who leave mid-process[6]. Experts agree that identifying and fixing roadblocks in processes like loan applications can greatly improve conversion efficiency.

Personalization drives engagement. Custom CTAs and risk-based recommendations aren't just nice-to-haves - they're game-changers. Personalized CTAs perform 202% better than generic ones, while risk-based recommendations can boost conversions by 25–50%[6]. These strategies reinforce the importance of leveraging user data effectively.

To optimize effectively, zero in on metrics like KYC completion rates, first funding, and 90-day retention. Tools like Amplitude for behavioral analytics, Optimizely for A/B testing, and Hotjar for user feedback can help you pinpoint problem areas and prioritize impactful changes. By focusing on the metrics that matter most, you can drive meaningful improvements.

FAQs

::: faq

Which conversions should a fintech app optimize first?

When it comes to fintech apps, early user interactions are crucial for building trust and encouraging engagement. Processes like onboarding and account setup - think KYC (Know Your Customer) and bank account linking - can often feel like hurdles, leading to high drop-off rates. To address this, it's essential to focus on trust signals, security assurances, and compliance transparency. These elements help ease user concerns and build confidence.

At the same time, simplifying these steps with clear instructions and intuitive, user-friendly forms can make a world of difference. A smoother, more straightforward process not only reduces friction but also boosts retention, keeping users engaged from the start. :::

::: faq

How can we reduce KYC drop-offs without risking compliance?

To reduce KYC drop-offs while staying compliant, prioritize creating a smoother user experience. Leverage automation to make the verification process faster, and break tasks into smaller, manageable steps using progressive disclosure. Be upfront about why specific information is required - clear communication builds trust and encourages users to complete the process. Striking the right balance between compliance and usability - such as eliminating redundant steps and simplifying workflows - can effectively decrease drop-off rates without sacrificing regulatory standards. :::

::: faq

What are the fastest trust signals to improve sign-ups?

When it comes to boosting sign-ups quickly, some trust signals work like a charm. These include prominently displaying security badges, featuring customer testimonials, using social proof (like reviews or user stats), and offering clear, transparent contact information. Together, these elements can instantly make your brand feel credible and trustworthy, encouraging users to take action. :::

Go deeper than any blog post.

The full system behind these articles—frameworks, diagnostics, and playbooks delivered to your inbox.

No spam. Unsubscribe anytime.